How to Fill Out Form 8949 for Crypto: A Step-by-Step Guide

May, 10 2026

May, 10 2026

Did you know that simply spending Bitcoin on a coffee can trigger a tax event? It sounds crazy, but under current US law, the Internal Revenue Service (IRS) treats cryptocurrency as property rather than currency. This means every time you sell, trade, or spend your digital assets, you have to calculate your profit or loss. That’s where Form 8949 comes in.

If you’re staring at this form and feeling overwhelmed, you aren’t alone. The IRS requires you to report every single disposal of crypto assets on Form 8949 before summarizing them on Schedule D. Missing even one transaction can lead to penalties, audits, or worse. Let’s break down exactly how to fill it out without losing your mind.

What Is Form 8949 and Why Do You Need It?

Form 8949, officially titled "Sales and Other Dispositions of Capital Assets," is the detailed ledger the IRS uses to verify your capital gains and losses. Think of it as the receipt book for your crypto transactions. While Schedule D gives the IRS the final totals, Form 8949 provides the granular data for each individual trade.

You need this form because the IRS has been cracking down hard on crypto non-compliance. Since issuing Notice 2014-21, which established that virtual currency is property, the agency has increased enforcement significantly. In fact, crypto-related enforcement actions jumped by over 300% between 2020 and 2022. If you sold any Bitcoin, Ethereum, or altcoins in 2025, or swapped tokens on a decentralized exchange, you likely need to file this form.

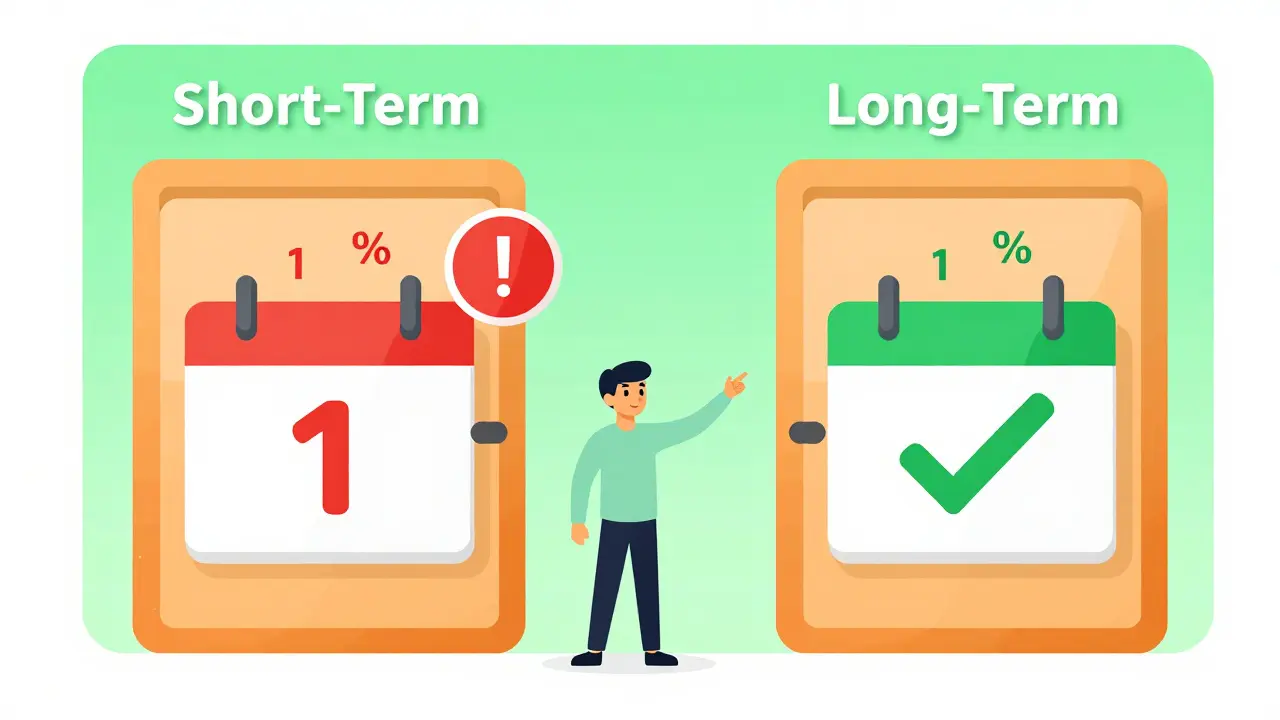

Short-Term vs. Long-Term: The Two Parts of Form 8949

The first thing you’ll notice is that Form 8949 is split into two distinct sections. Getting this right matters because it changes your tax rate.

- Part I: Short-Term Capital Gains and Losses. Use this section for assets you held for one year or less. These gains are taxed at your ordinary income tax rates, which can range from 10% to 37% depending on your total income bracket.

- Part II: Long-Term Capital Gains and Losses. Use this section for assets held for more than one year. These enjoy preferential tax rates of 0%, 15%, or 20%, making holding onto your crypto longer potentially much cheaper in terms of taxes.

To decide which part a transaction belongs in, look at the date you acquired the asset versus the date you disposed of it. If the gap is 365 days or fewer, it’s short-term. If it’s 366 days or more, it’s long-term.

Filling Out the Columns: A Step-by-Step Breakdown

Once you’ve decided whether a transaction goes in Part I or Part II, you need to fill in the specific columns. Here is what each column asks for:

- Description of Property: Don’t just write "Bitcoin." Be specific. Write "0.5 BTC" or "10 ETH" so the IRS knows exactly what was sold.

- Date Acquired: The exact date you bought or received the crypto.

- Date Sold: The exact date you sold, traded, or spent the crypto.

- Sales Price: The fair market value of the crypto at the time of sale. If you swapped Bitcoin for Ethereum, this is the dollar value of the Ethereum you received.

- Cost Basis: What you originally paid for the crypto, including any fees. This is crucial because it determines your gain or loss.

- Code (Column f): Leave this blank unless you need to adjust the gain or loss (for example, if you claimed a loss previously).

- Gain or Loss: Subtract your Cost Basis (Column e) from your Sales Price (Column d). This is your taxable amount.

Remember, the IRS explicitly states you must report all transactions, even those with a $0 gain or loss. Skipping small trades is a common mistake that triggers audits.

Boxes A, B, and C: Which One Are You?

Within Part I and Part II, you’ll see three boxes labeled A, B, and C. Your choice depends on whether your exchange reported your basis to the IRS.

| Box | When to Use It | Typical Scenario |

|---|---|---|

| A | Basis was reported to the IRS | You received a Form 1099-B from Coinbase or Binance showing your cost basis. |

| B | Basis was NOT reported to the IRS | Your exchange sent you a 1099-B but didn't include cost basis info, or you used a smaller platform. |

| C | No statement was received | You traded on a decentralized exchange (DEX), used a personal wallet, or mined crypto. |

Most major centralized exchanges now report gross proceeds to the IRS. However, they often don’t report accurate cost basis information yet. This means many taxpayers still fall into Box B or C, requiring manual calculation of their gains and losses.

Calculating Cost Basis: FIFO, LIFO, or Specific ID?

One of the trickiest parts of Form 8949 is determining your cost basis. Did you buy that Bitcoin in 2021 when it was $30,000, or in 2023 when it was $25,000? The method you choose affects your tax bill.

The IRS allows several methods, but Specific Identification is often the most tax-efficient for crypto traders. With Specific ID, you literally point to the exact coin you sold. For example, if you want to minimize taxes, you might choose to sell the coins you bought at the highest price first. To use this method, you must keep meticulous records and document your choice consistently.

If you don’t specify, the IRS generally assumes you used FIFO (First-In, First-Out). This means the first coins you bought are the first ones considered sold. This can sometimes result in higher taxes if your early purchases were made at lower prices, leading to larger gains.

Common Mistakes That Trigger Audits

I’ve seen too many people get caught off guard by these simple errors. Avoid them to keep the IRS happy:

- Ignoring Wallet Transactions: Just because you didn’t use Coinbase doesn’t mean you’re safe. Transfers between wallets, staking rewards, and DeFi swaps are all taxable events.

- Mismatched Dates: Ensure the dates on your Form 8949 match the dates on your exchange statements. Even a one-day discrepancy can raise red flags during an audit.

- Forgetting Fees: Trading fees are part of your cost basis. Including them lowers your taxable gain. Make sure you add these to Column E.

- Omitting Zero-Gain Trades: As mentioned, every disposal counts. Don’t skip trades just because you broke even.

Using Crypto Tax Software to Simplify the Process

If you have more than 50 transactions, doing this manually is a nightmare. Most serious traders use crypto tax software like Koinly, CoinLedger, or CoinTracker. These tools connect to your exchanges and wallets via API, automatically importing your transaction history.

They then apply your chosen cost basis method (like Specific ID) and generate a ready-to-file Form 8949. According to recent surveys, using such software can cut preparation time from 15+ hours to just a few hours. Given the complexity of DeFi and cross-chain swaps, investing in reliable software is often worth the cost to avoid costly penalties.

What’s Coming in 2026?

Good news for future filers: the landscape is changing. Starting with tax year 2025 (filed in 2026), the IRS introduced Form 1099-DA. This new form will require exchanges to report both gross proceeds and cost basis information directly to the IRS. By 2026, full cost basis reporting will begin, which should drastically reduce the manual entry required for Form 8949.

Until then, however, you’re on your own. Keep your records clean, double-check your calculations, and don’t ignore those small trades.

Do I need to file Form 8949 if I only bought crypto and held it?

No. Buying crypto with fiat currency (like USD) is not a taxable event. You only file Form 8949 when you dispose of the asset-meaning you sell it, trade it for another crypto, or spend it on goods and services.

What happens if I forget to report a small crypto trade?

The IRS matches data from exchanges (via Form 1099-K and 1099-B) against your return. If you miss a trade, you could face penalties of 20% of the underpayment or up to 75% in cases of fraud. It’s always better to report everything accurately.

Can I use the average cost method for crypto?

Generally, no. The IRS does not allow the average cost method for individual cryptocurrency holdings. You must use FIFO, LIFO, or Specific Identification. Using average cost can lead to rejection or audit.

How do I report staking rewards on Form 8949?

Staking rewards are taxed as ordinary income at the fair market value when you receive them. When you later sell or trade those staked coins, you report the disposal on Form 8949, using the value at receipt as your cost basis.

Is Form 8949 mandatory for all crypto users?

Yes, if you have had any taxable dispositions of cryptocurrency during the tax year. This includes sales, exchanges, and payments. Even if you have a net loss, you must file the form to claim the deduction.

Bronwen Butler

May 11, 2026 AT 11:56the whole premise of this guide is flawed because the system itself is broken. nobody should have to spend hours filling out forms for digital assets that are treated like property when they function as currency in practice. it's a bureaucratic nightmare designed to crush innovation and punish everyday users who just want financial freedom. the irs doesn't care about your coffee purchase they care about compliance theater.

Ellie Riddell

May 12, 2026 AT 14:28oh look another tax form guide. how thrilling. i suppose we should all be grateful that the government allows us to keep our money after they've taken their cut. the irony is palpable here. you're explaining how to report losses on an asset class that exists outside their control while they try to drag it into their ledger. classic move.

Pauline Larocco71

May 12, 2026 AT 19:33thats so true though i feel for everyone dealing with this. its really overwhelming to think about every single transaction being tracked. i made a mistake once and forgot to log a small swap and now im worried. maybe using software is the best way to go so you dont have to stress about it. hope everyone finds peace in their taxes lol

John Gonzalez Bentham

May 14, 2026 AT 10:15you people are idiots if you think software fixes anything. the software is just another layer of incompetence. specific id is the only way but most of you cant even track your own wallets let alone do tax optimization. stop complaining and start learning or get audited and cry about it later. its that simple.

Tobias Gjerlufsen

May 15, 2026 AT 15:17the entire structure of capital gains taxation on crypto is a philosophical failure of modern economic theory. treating decentralized tokens as static property ignores the fluid nature of value exchange in a post-fiat world. you are essentially paying a penalty for participating in a more efficient market mechanism. the irs is clinging to outdated concepts because they cannot comprehend the underlying technology.

Ruben Michel

May 17, 2026 AT 09:57one must appreciate the sheer elegance of Form 8949 despite its tedious nature. it serves as a rigorous test of one's organizational prowess and attention to detail. those who fail to master it are simply unprepared for the complexities of high-level financial management. precision is not merely recommended; it is the hallmark of the discerning investor.

Jerry CUNNINGHAM SR

May 18, 2026 AT 07:27it is important to remember that following these guidelines ensures fairness for everyone in the community. by accurately reporting our transactions we contribute to a stable economic environment. i encourage all readers to take the time to understand their obligations and seek professional advice if needed. let us support each other in navigating these challenges responsibly.

Destiny Kilby

May 19, 2026 AT 14:15i always find these posts helpful because they clarify things that seem confusing at first glance. it makes me feel better knowing others are struggling too. please keep sharing tips because it helps reduce anxiety around filing time. thanks for breaking it down simply

beti macedo

May 21, 2026 AT 06:10you can do this! many people find the process daunting at first but with patience and careful planning everything will work out fine. believe in yourself and take it one step at a time. the effort you put in now will pay off later when you file correctly. stay positive and focused on the goal ahead.

Amit Varpe

May 21, 2026 AT 21:10india does not have such stupid forms :P