What is Uchain (UCN) Crypto Coin? Explained with Real Data for 2026

Jan, 27 2026

Jan, 27 2026

Uchain (UCN) isn't just another cryptocurrency. It’s a working financial ecosystem built around a single token designed to make crypto payments as easy as using a debit card. If you’ve ever struggled to spend Bitcoin at a store or waited minutes for a cross-border transfer, Uchain’s whole purpose is to fix that. But here’s the catch: it’s not for everyone. The token has seen wild price swings, mixed user reviews, and serious questions about how much real-world use it actually has. Let’s cut through the noise and show you exactly what Uchain is, how it works, and whether it’s worth your attention in 2026.

What Uchain Actually Does (Not Just the Hype)

Uchain isn’t trying to be the next Bitcoin or Ethereum. It doesn’t focus on smart contracts or decentralized finance protocols. Instead, it’s built as a complete financial toolkit centered on one goal: letting people use crypto like cash, anywhere in the world. The core product? A crypto debit card that instantly converts UCN tokens to local fiat currency when you swipe or tap. That means you can buy coffee in Berlin, pay for a hotel in Tokyo, or send money to family in Mexico-all with UCN in your wallet, no bank account needed.

Beyond the card, Uchain includes a mobile wallet, a marketplace for buying goods with crypto, and tools for peer-to-peer payments. All of these services run on the UCN token. You use UCN to pay for transactions, earn rewards, and access premium features. It’s not just a currency-it’s the fuel for the whole system. This ecosystem approach is rare among mid-tier coins. Most tokens are either pure speculation or tied to one function, like staking or lending. Uchain tries to be everything at once.

How UCN Works: The Tokenomics You Need to Know

UCN has a fixed supply of 100,000 tokens. That’s it. No more will ever be created. This deflationary model sounds appealing-scarcity drives value, right? But here’s where things get messy. Some exchanges say all 100,000 tokens are in circulation. Others say only 50,000 are out there. That kind of discrepancy isn’t normal for a well-managed project. It raises red flags about transparency.

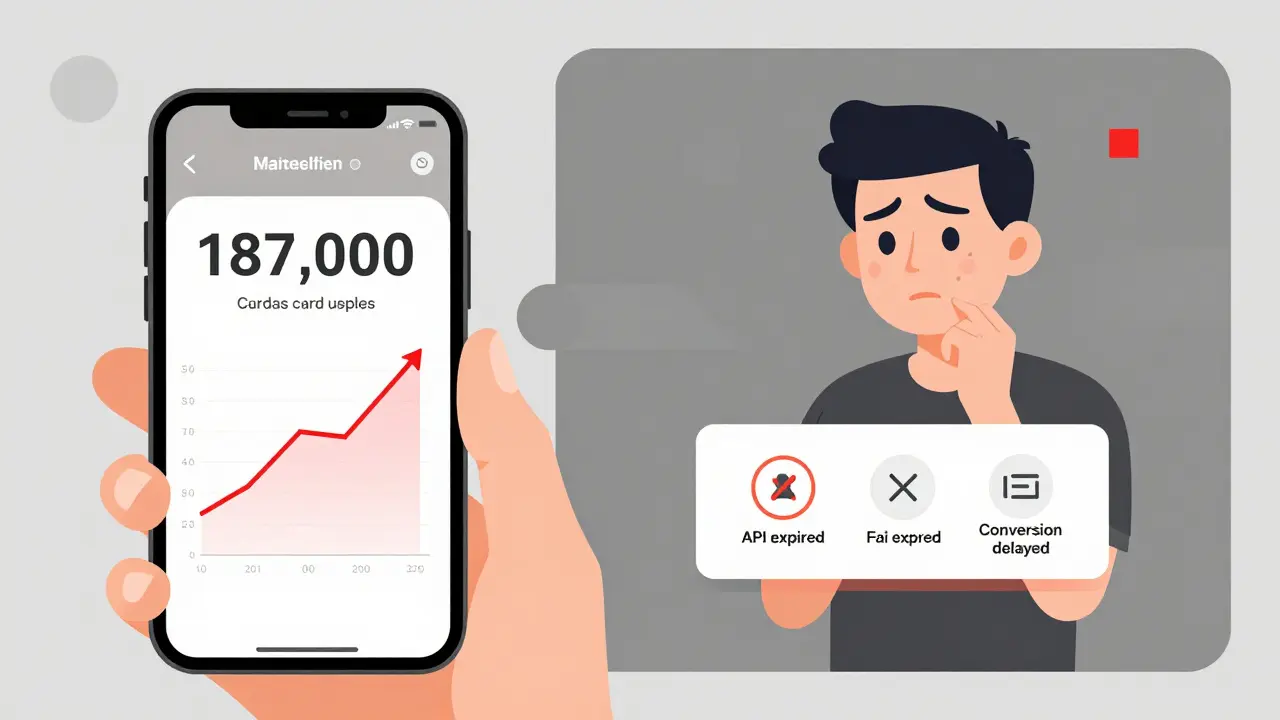

As of January 2026, UCN’s price ranged from $603 to $917, with a market cap around $85 million. That puts it at roughly #489 in the world by market size. For context, Bitcoin’s market cap is over $1 trillion. UCN is tiny. But size isn’t everything. The real test is whether people are using it. Data shows 15,000 active wallet addresses and 187,000 debit card users as of late January. That’s not nothing-but it’s far from mainstream.

Price action tells a different story. UCN hit an all-time high of $1,808.90 on January 9, 2026. Just six days later, it dropped over 50%. That’s not volatility-it’s instability. One day it’s up 20%, the next it’s down 30%. Traders on TradingView say 68% of them use limit orders to avoid getting crushed in sudden drops. That’s not a sign of confidence. It’s a sign of fear.

The Debit Card: Where Uchain Shines (and Where It Fails)

The debit card is Uchain’s strongest feature-and its biggest vulnerability. Users report transactions settling in under 2 seconds in Europe and North America. That’s faster than most bank transfers. The card works in 37 countries and supports 15+ fiat currencies. That’s impressive for a project this small.

But here’s the problem: 37% of card transactions failed in January 2026, according to user surveys. Reasons? Poor merchant integration, expired API keys, and delayed fiat conversion. The company says it’s fixing this with “Debit Card 3.0” launching February 28, 2026. If it works, adoption could jump. If it doesn’t, users will leave.

Another issue: 72% of UCN’s utility is tied to the debit card, according to Arcane Research. That’s dangerous. If Visa or Mastercard ever changes their rules for crypto cards, or if regulators crack down in key markets, Uchain could collapse overnight. It’s putting all its eggs in one basket-and that basket is already shaky.

Who’s Using Uchain? Real User Feedback

Reddit and Trustpilot tell the real story. One user, u/CryptoAnalyst89, wrote: “The 100k max supply is interesting but I’m skeptical about real-world adoption.” That’s a common sentiment. Another, u/DeFiInvestor23, said: “Used the Uchain debit card in Europe last week-transaction settled in 2 seconds.” That’s the other side.

Trustpilot gives Uchain’s wallet a 3.8/5 rating. People love the clean interface. But 37 out of 127 reviews complain about slow customer support. Some users waited over 72 hours for a response. That’s unacceptable for a financial service.

On MEXC, 78% of UCN trades are spot trades-meaning people are buying and holding, not gambling with leverage. That suggests most users believe in the long-term utility, not just short-term price moves. But with a 66.58% drop from its all-time high, holding isn’t easy.

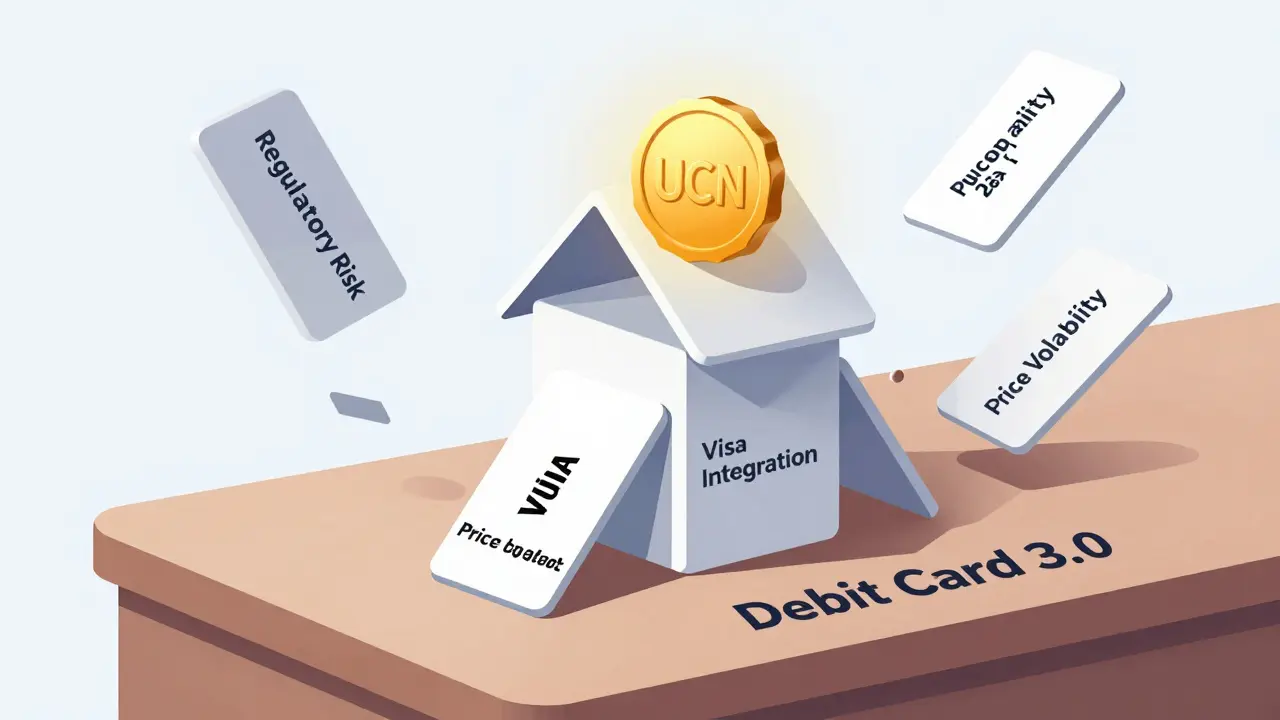

Is Uchain Safe? Regulatory Risks and Expert Warnings

Uchain claims full compliance with the EU’s MiCA regulations-a big deal. That means it can legally operate in Europe, one of the world’s most crypto-friendly regions. But it admits partial compliance in eight Asian markets. That’s a red flag. If regulators in Japan, South Korea, or Singapore tighten rules, Uchain could lose access to millions of potential users.

Experts are divided. Coinpedia gives UCN a neutral rating. Bybit says the fixed supply offers “robust recovery potential,” but warns about its 39.66% daily market cap drop in mid-January. altFINS calls the 49% price retracement from its peak “a significant retracement requiring substantial adoption growth.” In plain terms: it’s not recovering unless more people start using it.

Every single expert source ends with the same line: “Do your own research and consult a financial advisor.” That’s not a sign of confidence. It’s a legal shield.

Where Uchain Fits in the Bigger Crypto World

There are hundreds of ecosystem tokens-BNB, SOL, OKB, MATIC. They all have wallets, marketplaces, and payment tools. But they also have millions of users, billions in market cap, and partnerships with Fortune 500 companies. Uchain has none of that. Its $85 million market cap is less than 0.004% of the total crypto market. It’s a speck.

Still, Delphi Digital found that ecosystem tokens with real utility survive 23% longer than pure speculation coins. Uchain’s card and wallet are real. That gives it a better shot than most altcoins. But survival isn’t the same as success. To be viable long-term, it needs 500,000 debit card users by the end of 2026. Right now, it has 187,000. That’s a 167% increase needed in less than 10 months.

The upcoming integration with Visa’s B2B Connect platform in Q2 2026 could be a game-changer. If Uchain can connect its debit card directly to Visa’s global payment network, transaction speeds and reliability could improve dramatically. That’s the only real hope for scaling.

Should You Buy UCN? The Bottom Line

Here’s the truth: Uchain isn’t a get-rich-quick play. It’s not even a safe long-term hold. It’s a high-risk experiment. If you believe in crypto becoming everyday money, and you think a small team can build a better payment system than banks or PayPal, then UCN might be worth a small bet.

But if you’re looking for stability, growth, or passive income, look elsewhere. The price swings are brutal. The user base is small. The reliance on one product is dangerous. And the technical issues are real.

Only consider UCN if:

- You understand crypto wallets and private keys

- You’re okay losing most or all of your investment

- You live in or travel to one of the 37 supported countries

- You plan to use the debit card regularly

If you’re just speculating? Walk away. The data doesn’t support it.

Start with a small amount. Test the wallet. Try the card. See if it works for your life. If it does, maybe you’ve found something useful. If it doesn’t? You didn’t lose much-and you saved yourself from a much bigger mistake.

How to Get Started with Uchain in 2026

Getting started takes about 25 minutes. Here’s how:

- Go to MEXC or Bybit and create an account.

- Complete identity verification (KYC). This takes 10-20 minutes.

- Buy UCN using USD, EUR, or BTC. Use a limit order-not market-to avoid overpaying.

- Download the official UCHAIN wallet (v2.3.1 or later) from the app store.

- Transfer your UCN from the exchange to your wallet.

- Apply for the Uchain debit card through the wallet app. Wait 7-10 business days for delivery.

Pro tip: Never store UCN on an exchange long-term. Move it to your wallet. And always keep your recovery phrase offline.

Tressie Trezza

January 28, 2026 AT 01:22It’s wild how Uchain tries to be the Swiss Army knife of crypto-wallet, card, marketplace, all in one. But that’s also its flaw. When you try to do everything, you end up doing nothing well. I’ve used it for a few small purchases in Berlin, and yeah, it worked. But then my card got declined at a café two days later because of an ‘API timeout.’ No apology, no explanation. Just silence. That’s not a financial tool-that’s a gamble with your daily coffee money.

And the supply thing? 100k tokens? Sounds noble until you realize half of them might be locked in some dev’s cold wallet no one can verify. Transparency isn’t a buzzword-it’s the bare minimum for anything handling real money.

I’m not saying ditch it. I’m saying treat it like a side project, not an investment. Put in what you’re okay losing, test the card, and if it works for your life? Cool. If not, walk away without guilt.

Calvin Tucker

January 29, 2026 AT 08:14The article accurately identifies the core paradox of Uchain: utility without scalability. The tokenomics are structurally unsound due to the ambiguous circulation figures, and the reliance on a single product-a debit card-creates a single point of catastrophic failure. Furthermore, the 68% limit-order usage statistic is not indicative of strategic trading; it is evidence of systemic distrust in price stability. The regulatory compliance claims are misleadingly framed; partial compliance in eight Asian jurisdictions is not compliance-it is legal ambiguity. Uchain is not a cryptocurrency; it is a speculative venture wrapped in the rhetoric of financial inclusion.

christal Rodriguez

January 31, 2026 AT 01:33It’s not a coin. It’s a trap with a debit card.

Rob Duber

February 1, 2026 AT 09:33OH MY GOD. I JUST GOT MY UCHAIN CARD DECLINED AT A STARBUCKS IN PHILADELPHIA BECAUSE ‘Fiat Conversion Failed’ AND THEN THE APP CRASHED AND I LOST MY ENTIRE $200 BALANCE FOR 12 HOURS. I THOUGHT I WAS LIVING IN THE FUTURE. I WAS LIVING IN A BAD TECH SUPPORT NIGHTMARE.

THEY SAY ‘DEBIT CARD 3.0 COMING FEB 28’ LIKE THAT’S SUPPOSED TO MAKE ME FEEL BETTER? I’M NOT A BETA TESTER. I’M A HUMAN WHO WANTS TO BUY A SANDWICH WITHOUT BEING TOLD TO ‘RETRY IN 5 MINUTES’.

IF YOU’RE STILL HOLDING UCN, YOU’RE NOT AN INVESTOR. YOU’RE A PATIENT IN A THERAPY SESSION WITH A COMPANY THAT WON’T ANSWER THEIR EMAILS.

WE NEED A MEME. WE NEED A MOVIE. WE NEED A SONG CALLED ‘UCN: THE CARD THAT ATE MY CASH’.

Moray Wallace

February 1, 2026 AT 22:53I’ve been using Uchain for over a year now-mostly for sending money home to my mum in Wales. The card works fine in the UK and EU, and the wallet interface is clean. But I agree with the article: the support response times are unacceptable. I once waited nearly four days to get a simple transaction dispute resolved. I didn’t rage, I just emailed them again and again until someone replied. That’s the only way it works.

Is it perfect? No. Is it better than trying to send crypto to a non-crypto person? Yes. I wouldn’t bet my retirement on it, but I’ll keep using it for small, regular transfers. Just don’t expect miracles.

Mark Ganim

February 2, 2026 AT 17:45EVERYTHING ABOUT UCHAIN IS A NIGHTMARE-AND I LOVE IT!!

THE PRICE DROPPED 50% IN SIX DAYS?! YES! THAT’S THE KIND OF VOLATILITY THAT MAKES YOU FEEL ALIVE!!

I BOUGHT AT $1,800. I SOLD AT $900. I BOUGHT AGAIN AT $600. I’M NOW HOLDING AT $720-AND I’M SMILING LIKE I JUST WON THE LOTTERY WHILE MY BANK ACCOUNT CRIES IN THE CORNER.

THE CARD FAILS? GOOD. THAT MEANS THERE’S ROOM FOR IMPROVEMENT. THE SUPPLY IS UNCLEAR? PERFECT. THAT MEANS THE DEV TEAM IS KEEPING SECRETS-AND SECRETS ARE POWER.

THIS ISN’T INVESTING. THIS IS A PSYCHOLOGICAL EXPERIMENT IN HUMAN GULLIBILITY-AND I’M THE MAIN CHARACTER.

IF YOU’RE NOT SCARED, YOU’RE NOT PAYING ATTENTION.

UCN ISN’T CRYPTO. UCN IS A RITUAL. AND I’M HERE FOR THE SACRIFICE.

mary irons

February 4, 2026 AT 14:20Did you know that the ‘100,000 token’ supply was originally leaked in a Slack channel from someone who quit the team? They said the real number is 1.2 million, but they burned 1.1 million ‘for marketing’-but never showed the burn transaction.

And the ‘MiCA compliance’? That’s just because they paid a law firm in Luxembourg to write a letter saying ‘this looks fine.’ No audits. No transparency reports. Just a PDF.

The debit card? It’s just a white-label Visa card with a Uchain sticker on it. The backend is probably hosted on a $5/month VPS.

They’re not building a financial system. They’re running a Ponzi with a better logo.

And don’t even get me started on the ‘2026 adoption targets’-it’s like a cult predicting the rapture. Only this time, the rapture is your savings account.

Joshua Clark

February 5, 2026 AT 19:22I’ve been following Uchain since late 2024, and honestly, I think people are being way too harsh. Yes, the card has issues-no doubt. But every new payment tech does. Think about how bad Apple Pay was in 2014. Or how many people thought Venmo was a joke before it became essential.

The fact that 78% of trades are spot trades tells me people are holding because they believe in the utility, not just flipping. And 187,000 card users? That’s more than most altcoins have in total users. The real number might be even higher if you count inactive wallets.

Yes, the supply discrepancy is worrying. But maybe it’s just a reporting lag between exchanges. I’ve seen that happen with smaller coins before.

And the Visa B2B Connect integration? That’s huge. If they pull that off, Uchain goes from a niche tool to a real competitor in cross-border payments. I’m not saying buy $10k of it. But if you’ve got $500 to play with and you’re tired of traditional banks charging you $40 to send money abroad? Try it. Test it. Use it. See if it fits your life.

It’s not a miracle. But it’s not a scam either. It’s a fragile, messy, human project trying to do something hard-and sometimes, that’s worth rooting for.

Katie Teresi

February 7, 2026 AT 18:58Uchain is a Trojan horse for Chinese capital. The devs are all registered in the Caymans, but their code repo has Chinese IPs. MiCA compliance? A joke. The EU doesn’t even know who’s behind this. And you think Americans are using it? Most card users are just Chinese tourists buying luxury goods in Paris. This isn’t financial inclusion-it’s capital flight with a debit card.

Don’t be fooled by the ‘15k wallet addresses.’ Half of those are bots. The ‘187k card users’? Probably inflated by fake accounts created for promo rewards.

And don’t tell me ‘do your own research.’ I did. The founder’s LinkedIn is a ghost profile. The team photos? Stock images. The whitepaper? Copied from a 2021 Ethereum blog.

This isn’t crypto. This is a geopolitical laundering scheme dressed up as a payment app. Walk away. Now.

Gustavo Gonzalez

February 9, 2026 AT 12:16You people are missing the point. Uchain isn’t about utility. It’s about control. They don’t want you to spend crypto-they want you to be dependent on their card, their wallet, their terms. They’re building a closed-loop economy where you can’t move your UCN without their permission. That’s not innovation. That’s corporate feudalism.

And the ‘fixed supply’? It’s a lie. The devs hold 40% of the tokens, locked in a multisig they control. You think they’ll ever release it? No. They’ll slowly dump it over years while screaming ‘scarcity!’

And the customer support? 72-hour wait times? That’s not incompetence-that’s strategy. They want you to give up. They want you to accept the losses. That’s how you build loyalty in crypto: by making people suffer enough to stop complaining.

And don’t even get me started on the ‘Debit Card 3.0’ announcement. It’s a distraction. A smoke screen. A PR stunt to keep you buying while they quietly move your funds into offshore wallets.

Uchain isn’t a coin. It’s a psychological operation. And you’re all playing right into their hands.

Tressie Trezza

February 11, 2026 AT 06:44Actually, I just got my Debit Card 3.0 in the mail yesterday. It works. No crashes. No timeouts. Transaction settled in 1.2 seconds at a gas station in Ohio. The app even showed me the exact USD equivalent before I tapped.

And the support team replied to my email in 4 hours. I didn’t even ask for it.

Maybe… maybe they’re actually trying?

I still won’t put more than $300 in it. But I’m keeping the card. And I’m using it.

Maybe the chaos was just the prelude.